2021 has been a remarkable year for the entire cryptocurrency industry. Bitcoin once again hit more highs, first breaking the psychological barrier of $50 000 and then notching an all-time high of $69 000, sparking hopes it could hit $100 000 or higher at some point. As expected, major support for Bitcoin came from institutional investors, who were increasingly buying up the world’s largest cryptocurrency amid the long-awaited approval of bitcoin futures ETFs by the US Securities and Exchange Commission (SEC). Let us recall that the first bitcoin-linked exchange-traded fund listed in the United States, the ProShares Bitcoin Strategy ETF, trading under the ticker BITO, became available on the New York Stock Exchange on 19 October 2021. Thanks to this event and other fundamental drivers, inflows into bitcoin products and funds have exceeded a record $6.4 billion in 2021.

The hype around Bitcoin ETFs revealed the desire of an entirely new class of investors to experience the benefits of investing in cryptocurrency as a legitimate asset. Many experts note that the launch of a fully legitimate bitcoin derivative demonstrates not only a special attitude of regulators to the cryptocurrency environment but also their readiness to move on towards creating a regulated market.

The above-mentioned fundamental backdrop was enough to send BTC to new highs, but the buyers failed to gain a foothold there. The initiative quickly shifted to sellers after optimism around the launch of the first Bitcoin ETF was completely wiped out by the negative reports of a possible default of highly indebted developer China Evergrande Group, whose liabilities exceed $300 billion.

A while ago, Evergrande’s representatives noted that there is no guarantee that the group will have sufficient funds to continue to perform its financial obligations, which basically meant that the Evergrande Group could declare bankruptcy. This news sparked contagion concerns across China’s property and banking sectors, threatening China’s “financial system and the overall economy”, making investors extremely cautious.

It may seem as though the Chinese developer has nothing to do with the cryptocurrency industry, but a deeper analysis suggests otherwise. Experts admit that Evergrande defaulting may trigger a collapse in investors’ trust in those stablecoins that play a vital role in the cryptocurrency ecosystem. It’s no secret that stablecoin issuers keep most of their assets in commercial and certificates of deposit. Since companies don’t provide detailed information on the composition of their investment portfolios, one may assume that many of those companies could face high risks associated with Chinese securities. Thus, Evergrande’s collapse may trigger a domino effect leading to new defaults that could affect the commercial paper in the portfolios of those stablecoin issuers.

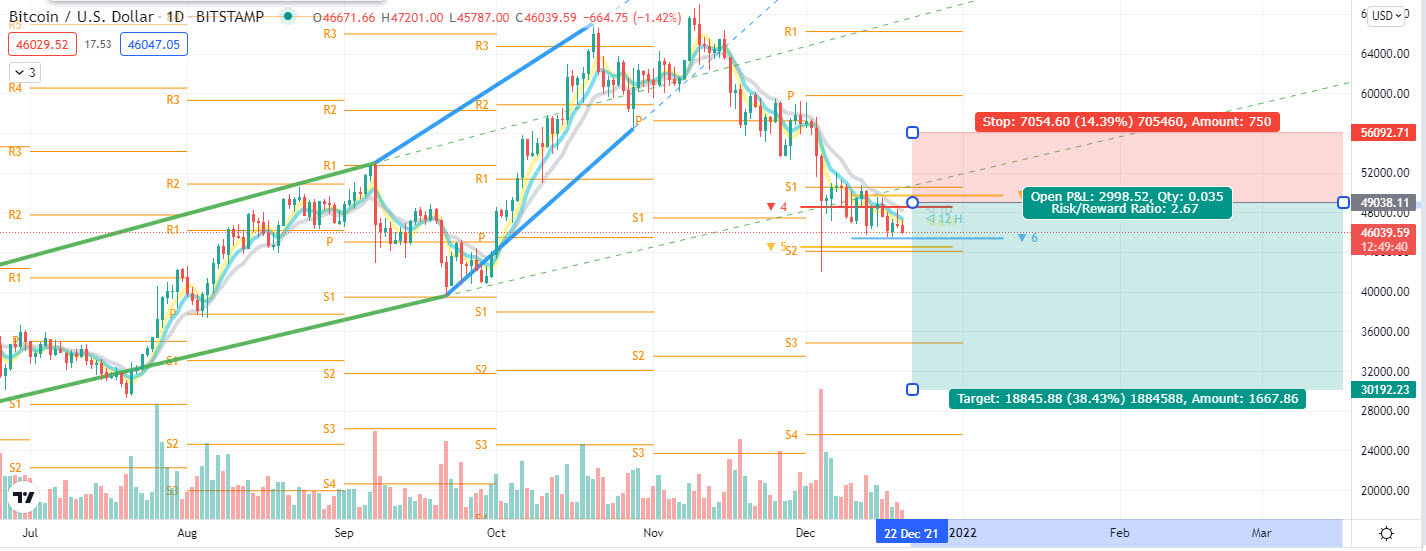

BTC/USD Chart

On December 9, Evergrande failed to meet its interest payments to international investors. Fitch Ratings downgraded the troubled Chinese property developer to a “restricted default”. “Restricted default” (‘RD’ rating) means that the company has experienced an uncured payment default on a material financial obligation but has not yet entered into bankruptcy filings, administration, receivership, liquidation, or other formal winding-up procedures, and has not otherwise ceased operating. Given that this could happen at any time, the cryptocurrency market could face yet another wave of aggressive sell-off. That being said, we recommend shorting BTC/USD with a target of $30 000.

Oil under pressure due to Omicron uncertainty

2021 has been a rather productive year for the entire oil market. Brent crude oil managed to take advantage of the global economic recovery, restoring its positions from $51.76 to $80 per barrel. Despite such an outstanding result, the bright future for oil buyers is yet in question.

A serious threat to the hydrocarbon industry comes from the deteriorating epidemiological situation worldwide. Coronavirus fears have been affecting the traders’ sentiment for 2 consecutive years. And although several pharmaceutical giants rolled out vaccines that have proved effective against COVID-19, the emergence of a new fast-spreading variant is highly likely to compromise some of the protection from the existing vaccines. Viruses mutate all the time, so it is not surprising that every time a new variant is discovered, the market goes straight into panic mode, with traders fearing another global recession and an inevitable drop in oil demand.

December 2021 was overshadowed by the emergence of a new coronavirus variant named “Omicron”. According to preliminary data, the new variant is highly contagious and is spreading significantly faster than Delta. It’s also resistant to current jabs. As soon as these fears were confirmed by a sharp increase in the number of daily confirmed cases in England, Austria and Germany, the market reacted accordingly. Traders, fearing that governments would introduce new restrictions, started to actively get rid of all risky assets, including oil. Against this backdrop, Brent crude oil dropped from $80 to $65.

The International Energy Agency revised down its global oil demand forecast for 2021 and 2022 by around 100,000 barrels per day (bpd) compared to last month’s assessment due to the new surge in coronavirus cases. The IEA said global oil demand was now expected to rise by 5.4 million barrels per day in 2021. The decrease in demand will occur amid the growing supply. Let us recall that in November, global production increased by 970 thousand barrels per day. U.S. crude oil production has been accelerating for the second consecutive month as U.S. shale producers are adding extra drilling rigs.

OPEC members are also ramping up production. Last month, the cartel raised its oil output by 285,000 barrels per day.

In the short term, additional oil may be released to the market from strategic oil reserves (SPR). On November 23, the US announced the release of 50 million barrels of oil from its reserves in an attempt to bring down soaring energy and petrol prices. The move will be made in conjunction with other major oil-consuming nations, including China, India, Japan, South Korea and the UK. This may add about 70 million to 80 million barrels of crude supply to the market, raising the global supply by another 200 thousand barrels per day.

That being said, sustained supply growth, coupled with weakening demand amid the ongoing COVID-19 pandemic, could result in the oil surplus of more than 1.5 million barrels in Q1 2022. During this time, sellers may well send Brent below $55.

Fed gives the green light to expensive dollar

This whole year, the US regulator has been trying to convince the markets that rising inflation, the national economy was facing, is only temporary since it was caused by temporary factors: deferred consumer demand, high oil prices, a shortage of personnel in the labor market and persisting supply problems. Nevertheless, time passed, and the long-awaited decline in inflation never happened. Moreover, the CPI, which measures how much Americans spend on goods and services, skyrocketed in November, reaching its highest rates since 1982, while the core CPI recorded the sharpest pickup since mid-1991.

After that, it became obvious that no one would believe in the tale of the “temporary nature” of high inflation in the United States. Once the Federal Reserve realized this, it decided to take action. Unfortunately, it took the Federal Reserve a whole year to realize all the risks associated with rising inflation expectations.

The regulator finally adjusted its monetary policy in December, at the very end of the outgoing year – “better late than never”, as they say. In an attempt to fight against the excessive inflation, the Fed decided to speed up its bond-buying taper. The central bank said that it will accelerate the reduction of its monthly bond purchases by $30 billion starting in January. Thus, the Fed will be buying $60 billion of bonds each month and will end its bond-buying program by the end of March.

It should be noted that withdrawing stimulus more quickly will allow the regulator to move to raising interest rates sooner. And while the FOMC has kept interest rates near zero for now, its new projections are very different from those announced less than a quarter ago. Let us recall that in September, half the members of the U.S. central bank’s policy-setting committee voted to wait until 2023 before raising interest rates. Now, the majority forecasts three interest rate hikes in 2022. This radical change in the Fed’s stance clearly demonstrates how rising inflation amid strong demand, persisting labor shortages and logistics problems can affect economic forecasts and the regulator’s monetary policy. Since these factors that triggered inflation in 2021 are still relevant, we can assume that the Fed will be forced to reduce its economic stimulus more rapidly. If these expectations are met, we can see the first rate hike as early as the first quarter of 2022.

That being said, the shift in the Fed’s rhetoric, as well as its dedication to finally deal with the rising inflation, will set a bullish trend in the dollar for the coming months. As a result, the U.S. dollar index (DXY) could test the psychological 100.00 level.

US stock market on the verge of collapse

2021 has become one of the most successful years for US stock indices. Thanks to the Fed’s soft monetary policy, US indices have hit multiple record highs. The S&P 500 broad market index added more than 30%, recovering from 3670 points to 4700. Remarkably, the Fed’s balance sheet grew by 20% over the same period, from $7.3 trillion to $8.7 trillion. Low rates motivated investors to look for instruments with higher returns. Companies were able to refinance at lower interest rates and buy back shares with borrowed funds, which generally created ideal conditions for businesses. However, all good things come to an end. The rapid rise in the Consumer Price Index forced the US regulator to abandon the unprecedented stimulus policy intended to help the United States mitigate the negative impact of the economic recession caused by the COVID-19 pandemic.

Now that the US regulator is forced to respond to elevated inflation risks and wind down its bond purchases at an accelerated pace, the US stock market may face not only increased volatility but also a potential collapse. As a result, the S&P 500 index may well plummet by more than 10%. This assumption is also well-grounded because the monetary policy tightening implies a reduction in the size of the Federal Reserve’s balance sheet.

Since the stock market rallied when the Fed bought bonds, there is every reason to believe that selling them back will trigger a downward trend in the market. Left without cheap liquidity, investors can start reallocating their funds to safer assets such as Treasury bonds. It didn’t make sense to do so before, as the general market euphoria fueled interest in risky assets. Things are different now. Global regulators are rushing to reduce stimulus to combat rising inflation, which dents investors’ confidence in the stock market.

Additional pressure on the S&P 500 index will keep coming from the deteriorating epidemiological situation around the globe. The new coronavirus variant is likely to hamper the global economic recovery. On the one hand, some countries impose new restrictive measures to contain its spread. On the other, it threatens to prolong the period of labor shortages and supply problems that cause inflation.

The US Centers for Disease Control and Prevention (CDC) warned of an imminent spike in the highly contagious new coronavirus variant. The World Health Organization (WHO) previously reported that Omicron spreads faster than other variants, and even though it may cause milder symptoms, it could still “overburden” healthcare systems. In its weekly epidemiological update, the WHO also mentioned the diminished efficacy of coronavirus vaccines against the Omicron variant. This is corroborated by the first large real-world study showing that two doses of the Pfizer-BioNTech vaccine offer reduced protection against Omicron. Currently, the new variant accounts for about 3% of cases in the United States, but the situation can deteriorate rapidly.

With that said, “short” positions in the S&P 500 look like a more promising investment decision. According to the consensus forecast, the S&P 500 index could test the 4,250 support as soon as in the first quarter of 2022.

What to do with the euro?

Market participants increasingly wonder if the European currency will be able to put up a decent fight against the dollar in the first quarter of 2022. Although optimists give an affirmative answer, referring to the euro’s status as a preferred funding currency, we hold a different opinion.

Firstly, the euro hasn’t been very popular among buyers for quite some time. The EUR/USD dynamics in 2021, when the pair slipped from 1.22 to 1.11, provides clear confirmation of this assumption. Secondly, in the new year, the situation for the euro can get even worse. New restrictions due to rising numbers of coronavirus cases caused by the Omicron variant, the ECB’s soft policy and depressing statistics indicate that the EU economy has narrowly avoided recession at the end of the outgoing year.

The only thing that could support the euro is a more hawkish stance of the European Central Bank in its fight against inflation, which is clearly out of control in the euro area. In December, the Eurozone consumer price inflation accelerated to 4.9%, the quickest annual reading since 1991.

It was logical to assume that the ECB would intervene and attempt to contain inflationary pressure. Instead, the regulator decided to leave its policy unchanged, leaving its benchmark refinancing rate unchanged at 0% at the end of the last meeting. In addition, the ECB made it clear that it will maintain its interest rate policy during the “transitory period”, in which inflation can move above target. In early July, the ECB adjusted its medium-term inflation target to 2% from the previous goal of “just below 2%”. According to the remarks of the ECB representatives, the ECB could meet the conditions to start raising rates only by the end of 2023, which basically means that the regulator will keep the rate around zero throughout 2022.

The ECB’s dovish rhetoric contrasts strongly with the Fed’s hawkish tilt. This divergence in the monetary policies of the two regulators is the main reason for the long-term weakness of the euro. Unlike the ECB, the Federal Reserve recognized the problem of high inflation and began to deal with it, announcing its plans to reduce its asset purchase program and raise its benchmark short-term rate three times next year.

The deteriorating epidemiological situation in Europe adds pressure on the euro. To battle a major rise in coronavirus cases the governments were forced to impose new restrictions ahead of the holidays. While many investors believe that strong vaccination rates will convince the authorities to refrain from introducing stricter measures, the Omicron’s fast spread raises concerns every day. With that said, the euro could face another period of fundamental weakness in the first quarter of 2022, which can cause the EUR/USD pair to test the 1.10 support.

In today’s fast-paced financial world, responsible trading is no longer a choice; it's a necessity. Technology has opened the markets to everyone, making access incredibly easy.

In today’s fast-paced financial world, responsible trading is no longer a choice; it's a necessity. Technology has opened the markets to everyone, making access incredibly easy. For active traders and investors, mastering the art of trading volatility is a crucial skill. Volatility, in financial terms, refers to the extent to which asset prices fluctuate over time. High volatility markets experience rapid price swings...

For active traders and investors, mastering the art of trading volatility is a crucial skill. Volatility, in financial terms, refers to the extent to which asset prices fluctuate over time. High volatility markets experience rapid price swings... The global financial market operates as a dynamic ecosystem, where understanding the connections between different market movements can provide invaluable insights for forecasting...

The global financial market operates as a dynamic ecosystem, where understanding the connections between different market movements can provide invaluable insights for forecasting... The forex market, also known as the foreign exchange market, stands as the largest and most traded financial market globally. FXTM is committed to equipping our clients...

The forex market, also known as the foreign exchange market, stands as the largest and most traded financial market globally. FXTM is committed to equipping our clients... Cryptocurrency trading has rapidly grown into a bustling and dynamic market that attracts traders from around the world. With the potential for significant profits...

Cryptocurrency trading has rapidly grown into a bustling and dynamic market that attracts traders from around the world. With the potential for significant profits...